Search Minnesota Property Records

Minnesota property records are public documents kept at the county level. Each of the state's 87 counties records deeds, mortgages, tax assessments, and property transfers through the County Recorder and Assessor offices. You can search many records online for free through county portals or the Beacon property search system. For certified copies of recorded documents, contact the County Recorder in the county where the property sits. The Minnesota Department of Revenue oversees property tax administration statewide while counties handle day-to-day recording and assessment work.

Minnesota Property Records Overview

Where to Find Minnesota Property Records

Property records in Minnesota are kept at the county level. The County Recorder in each of the state's 87 counties records and maintains documents related to real property. These include deeds, mortgages, mortgage satisfactions, liens, plats, and other instruments that affect title or ownership. The Recorder is the official custodian of these documents. Staff can provide copies in person, by mail, or through online portals where they exist.

The Minnesota Department of Revenue provides resources and oversight for property tax administration across the state. Their site at revenue.state.mn.us/property-taxes serves homeowners, renters, and county administrators. The department provides data, guidance, and forms for property tax refunds, exemptions, and valuation standards. Counties use these state guidelines when setting values and collecting taxes locally. The department also publishes annual property tax data reports that let you compare values and rates across all 87 counties.

The Minnesota Department of Revenue's property taxes portal at revenue.state.mn.us serves as the central hub for property tax resources across the state.

The portal is available in English, Spanish, Hmong, and Somali to reach the full range of Minnesota property owners and administrators.

The County Assessor sets the estimated market value and classification for every parcel in its county. Values are set as of January 2 each year. Valuation notices go out in late February or early March. If you disagree with your assessed value, you can appeal to the Local Board of Appeal and Equalization. That board meets each spring. Further appeals go to the County Board and ultimately to the Minnesota Tax Court, which handles property tax cases independently of the regular court system.

Note: For recorded documents like deeds and mortgages, contact the County Recorder. For assessed values and tax data, contact the County Assessor. Both offices are typically located in the county courthouse or county administrative building.

How to Search Minnesota Property Records Online

Many Minnesota counties offer free online access to property records through the Beacon system, run by Schneider Geospatial. You search by parcel ID, owner name, or address. Results include assessed values, sales history, building characteristics, and current tax status. The interface uses an interactive map with parcel boundaries and aerial imagery. Basic searches are free and need no login for standard public data.

Not every county uses Beacon. Anoka County provides online document search through the iDoc system at idoc.marketspan.com/Anoka. Carlton County uses both Laredo and LandShark GIS for records and parcel mapping. Becker County offers LandShark at becker-county-landshark.gisworkshop.com. Each system works a bit differently, but all give free public access to basic property data. For document images or certified copies, contact the County Recorder directly. Some counties offer subscription access for frequent searchers or title professionals.

The PRISM system at the Minnesota Department of Revenue shows how counties submit parcel-level data annually for statewide tracking and analysis.

PRISM stands for Property Record Information System of Minnesota. Each county submits four rounds of data per year, with deadlines in April and September. PRISM data includes parcel IDs, estimated market values, taxable market values, net tax capacity, and property classifications for every parcel in the state.

For older records not in digital form, visit the County Recorder in person. Most counties have digitized documents back to the 1980s or 1990s. Records before that era may be on paper, microfilm, or bound ledgers and require staff assistance to locate. Call ahead before making the trip so you know what to expect and whether the office can pull what you need during your visit.

Types of Minnesota Property Records

Minnesota property records fall into two main groups. Recorded documents are kept by the County Recorder. Assessment records are maintained by the County Assessor. Both are public, and most can be viewed without giving a reason for your request. The type of record you need determines which office you contact.

Recorded documents cover the full range of instruments that affect title or ownership. The County Recorder indexes all conveyances under Minnesota Statutes Chapter 507, maintaining entries for each document's date, parties, property description, and document type. Modern county recorders use computer databases that allow name, date, and document-type searches. Electronic recording is available in many counties through approved vendors, making it possible to file documents without a trip to the courthouse.

- Warranty deeds and quit claim deeds

- Mortgages and mortgage satisfactions or releases

- Federal and state tax liens

- Mechanic's liens and UCC filings

- Plats and surveys

- Well disclosure certificates

- Court judgments affecting real property

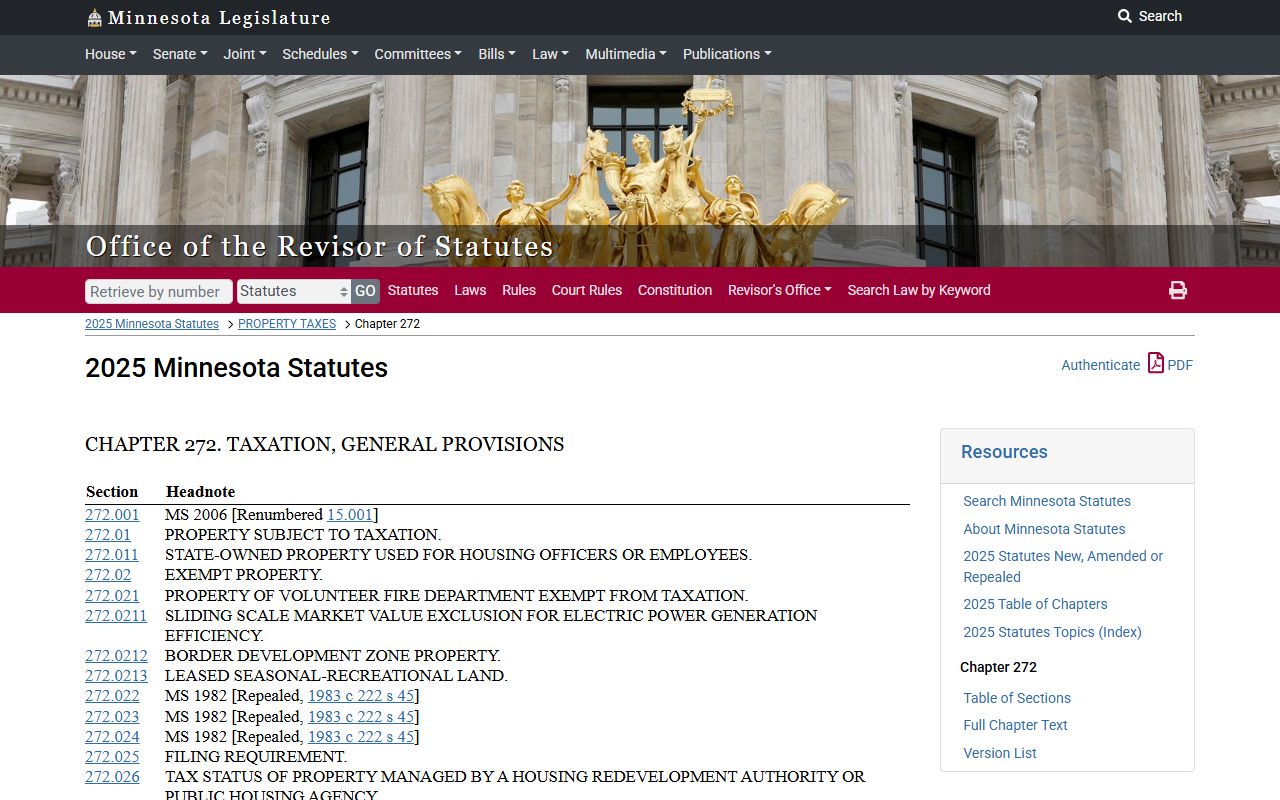

Assessment records show how the county has valued and classified each parcel. This includes the estimated market value, taxable market value, and the property's classification. Under Minnesota Statutes Chapter 272, all real and personal property in the state is taxable unless specifically exempt. Exempt categories include public schoolhouses, churches, public hospitals, academic institutions, and charitable organizations that meet state criteria. Wetlands and native prairie lands are also exempt. Wind energy conversion systems and solar energy generating systems carry partial exemptions.

Chapter 272 of the Minnesota Statutes sets the full scope of what property is taxable and what qualifies for exemption across all 87 counties.

Section 272.115 requires a certificate of value to be filed with the county when real property transfers. The certificate records the sale price and is used in deed tax calculations at the time of recording.

Minnesota's Two Property Recording Systems

Minnesota uses two separate systems for recording real property: the abstract system and the Torrens system. Most land in the state falls under the abstract system. Some counties, particularly in the Twin Cities metro area, also use Torrens registration. A given parcel can only be under one system at a time, but a single county may have both depending on how individual properties were registered over time.

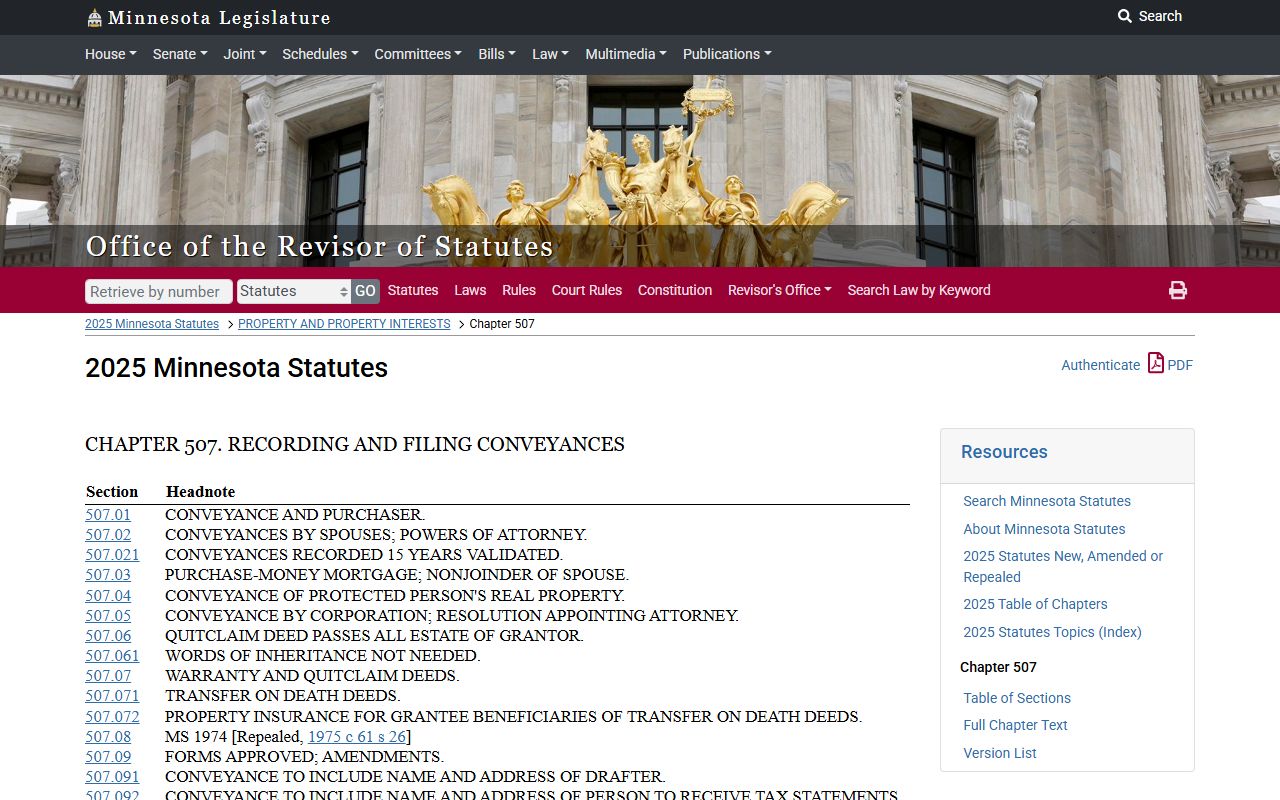

Under the abstract system, documents are recorded with the County Recorder and governed by Chapter 507. Recording creates a public record and puts the world on notice of the transaction. Section 507.24 requires the county recorder to keep a general index of conveyances listing the date of registration, names of the parties, and a description of the property. The county recorder may maintain this index electronically. Title to abstract property is tracked through a chain of recorded documents going back to the original grant of land.

Chapter 507 of the Minnesota Statutes governs recording of conveyances, including acknowledgment requirements, electronic recording rules, and the county recorder's indexing obligations.

Section 507.27 allows county recorders to reproduce instruments by photographic or other means, and those reproductions are as legally effective as the originals for all purposes including evidence in court.

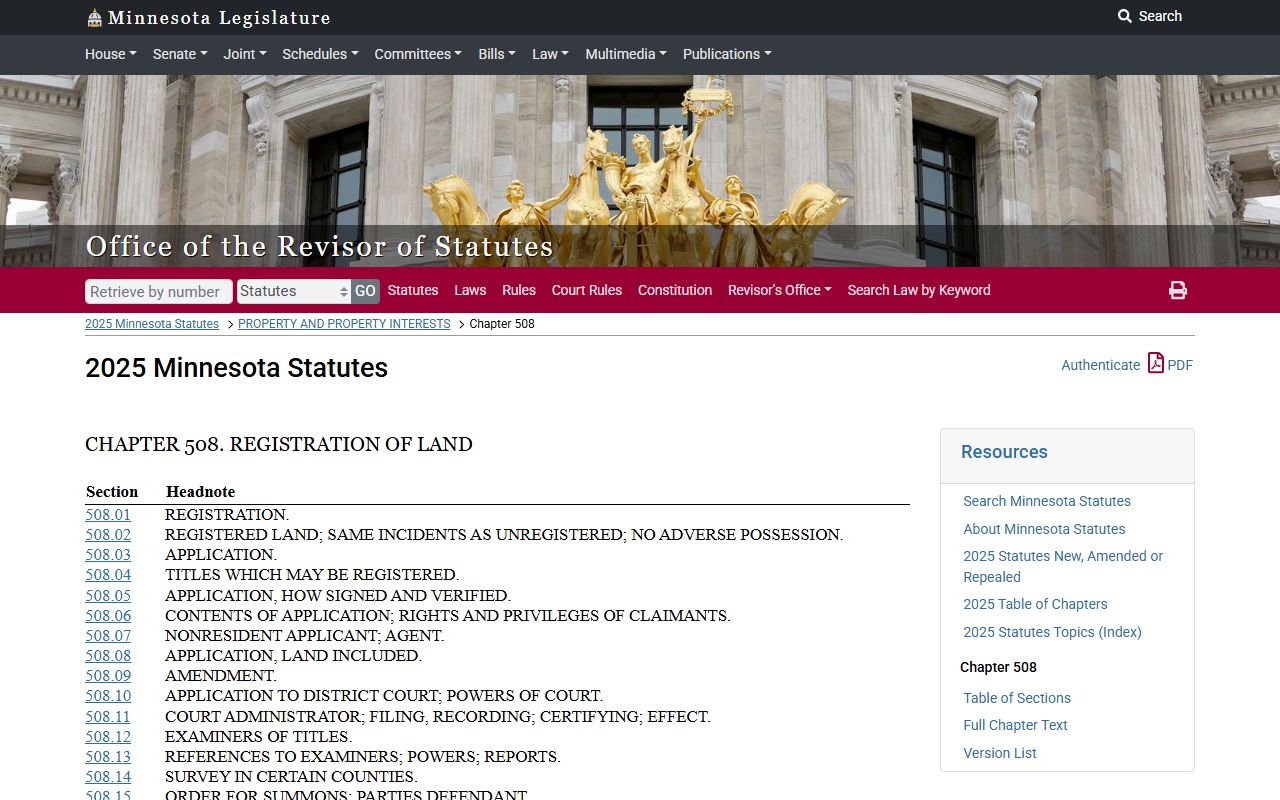

The Torrens system is governed by Chapter 508. Under Torrens, land is registered through a court proceeding. Once registered, the Registrar of Titles issues a Certificate of Title. That certificate is the authoritative record of ownership. Every subsequent transaction is filed with the Registrar, not recorded with the Recorder. No lien or encumbrance is valid against Torrens land unless it is noted in the Registrar's office. Chapter 508 describes this as "indefeasible title," meaning the certificate itself is the title. Getting land into the Torrens system typically costs over $1,000 including court fees. Once registered, ongoing Torrens transactions use the standard $46 filing fee.

Chapter 508 of the Minnesota Statutes governs the Torrens title registration system, under which a Certificate of Title issued by the Registrar is received in all courts as definitive evidence of land ownership.

Section 508.47 covers subsequent registration of Torrens land and the process for filing transactions after the initial certificate of title is issued.

Minnesota Property Tax Assessments

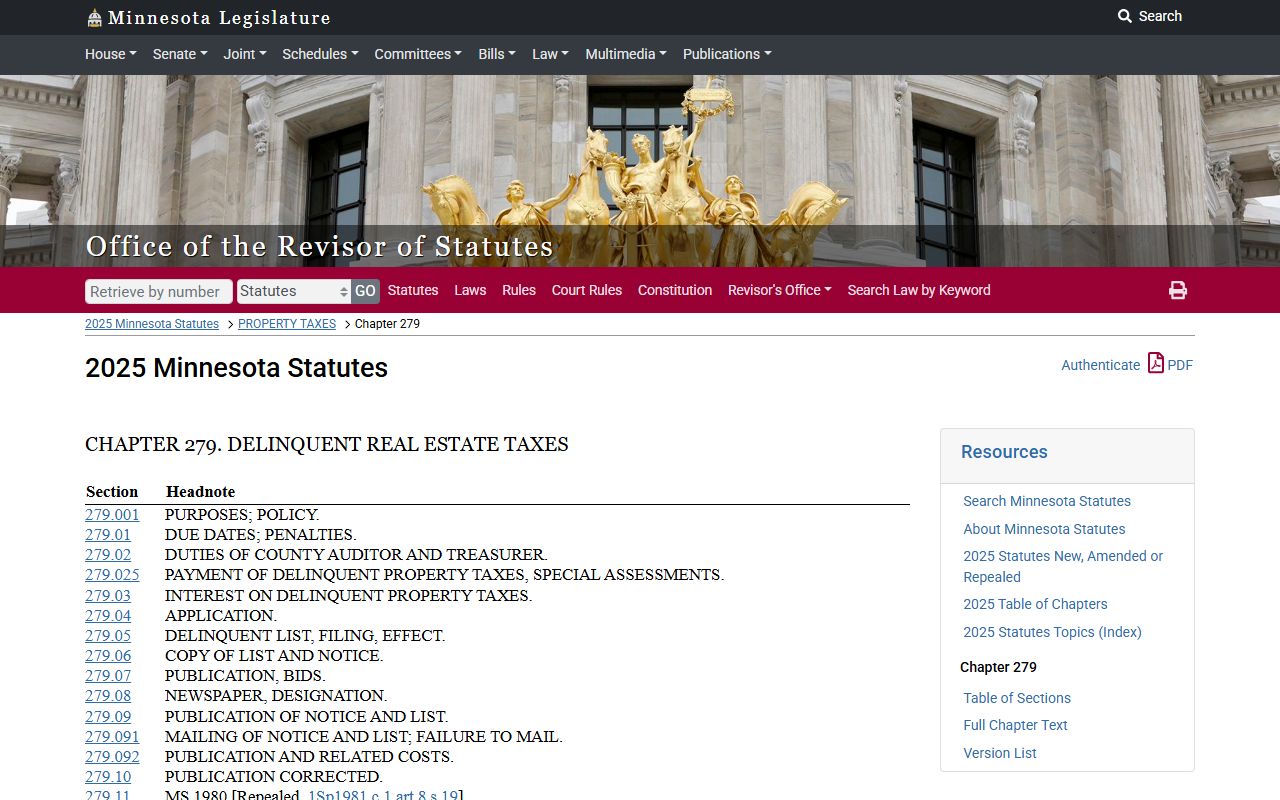

Property taxes in Minnesota fund local services including schools, roads, and public safety. Taxes come due in two installments. The first half is due May 15. The second half is due October 15. Taxes become delinquent on January 1 of the following year under Chapter 279. Delinquent taxes accrue interest at rates set by statute, typically 9 to 10 percent per year. If taxes remain unpaid for three years, the property enters tax forfeiture proceedings and can eventually be sold by the county.

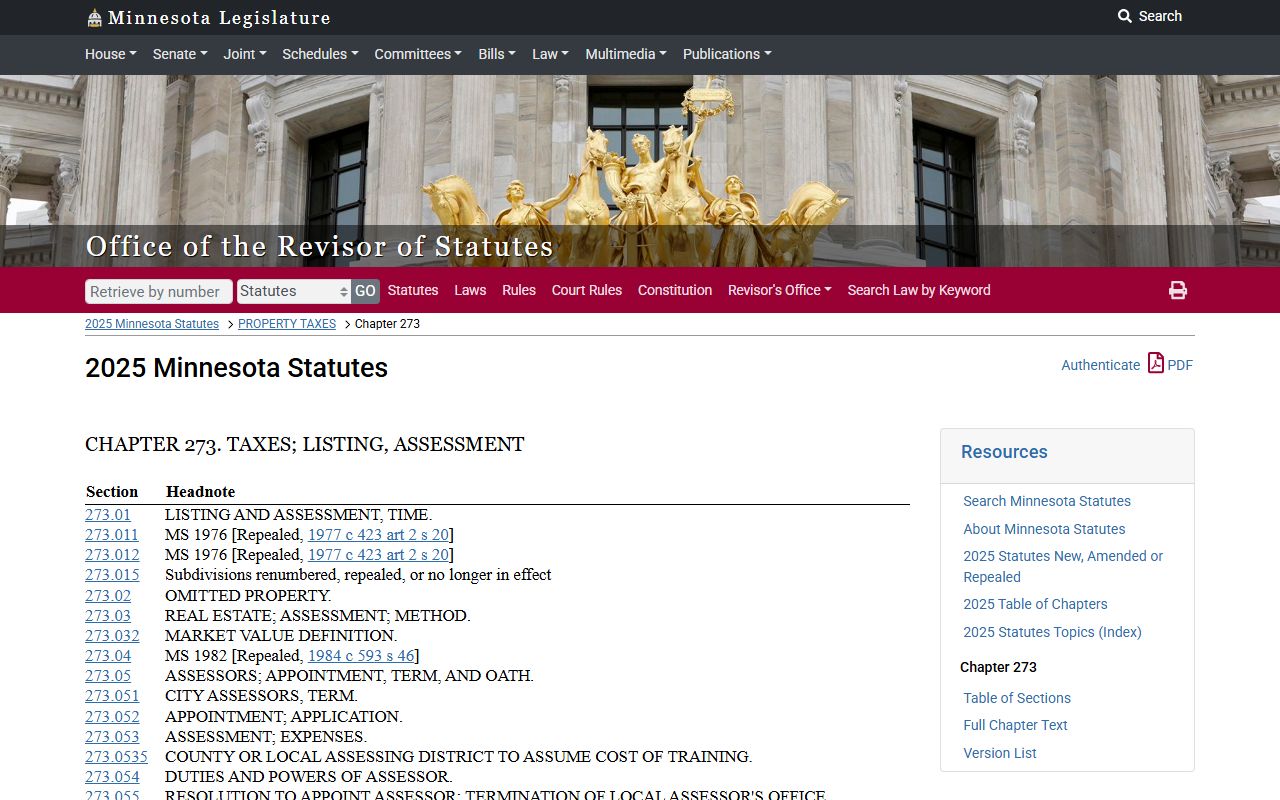

Property classifications under Minnesota Statutes Chapter 273 determine the rate applied to each parcel's market value. Residential homestead property pays 1.00% of the first $500,000 in estimated market value, and 1.25% on anything above that. Commercial and industrial property pays 1.50%. Agricultural homestead pays 0.50% on the first tier. Low-income rental property qualifies for a 0.75% to 1.25% rate. These classification rates produce the net tax capacity, which local taxing districts use with their levy rates to calculate the actual tax owed on each parcel.

Chapter 273 sets all classification rates and assessment standards for Minnesota property. The state revisor's page shows the full statute text including all property class definitions and rate structures.

The State Board of Equalization requires assessed values to fall between 90% and 105% of actual market value. Counties that fall outside that band are subject to state-ordered adjustments to their assessment rolls.

Chapter 279 sets the tax payment schedule and delinquency rules for real estate taxes in Minnesota, including interest and penalty rates for past-due amounts.

Property owners who pay before May 15 avoid late fees on the first half. The October 15 deadline applies to the second half. Larger properties exceeding 50,000 acres follow a three-installment schedule with different due dates.

Recording Fees for Minnesota Property Records

The standard recording fee in Minnesota is $46.00 for the first page of any document and $4.00 for each additional page. This covers deeds, mortgages, satisfactions, liens, and most other instruments filed with the County Recorder. Plats cost $56.00. Well disclosure certificates run $46.00 to $54.00 depending on the county. Documents with multiple titles cost $46.00 per title. Certified copies typically cost $10.00 plus per-page copy fees. Non-certified copies run $1.00 to $2.00 per page at most offices.

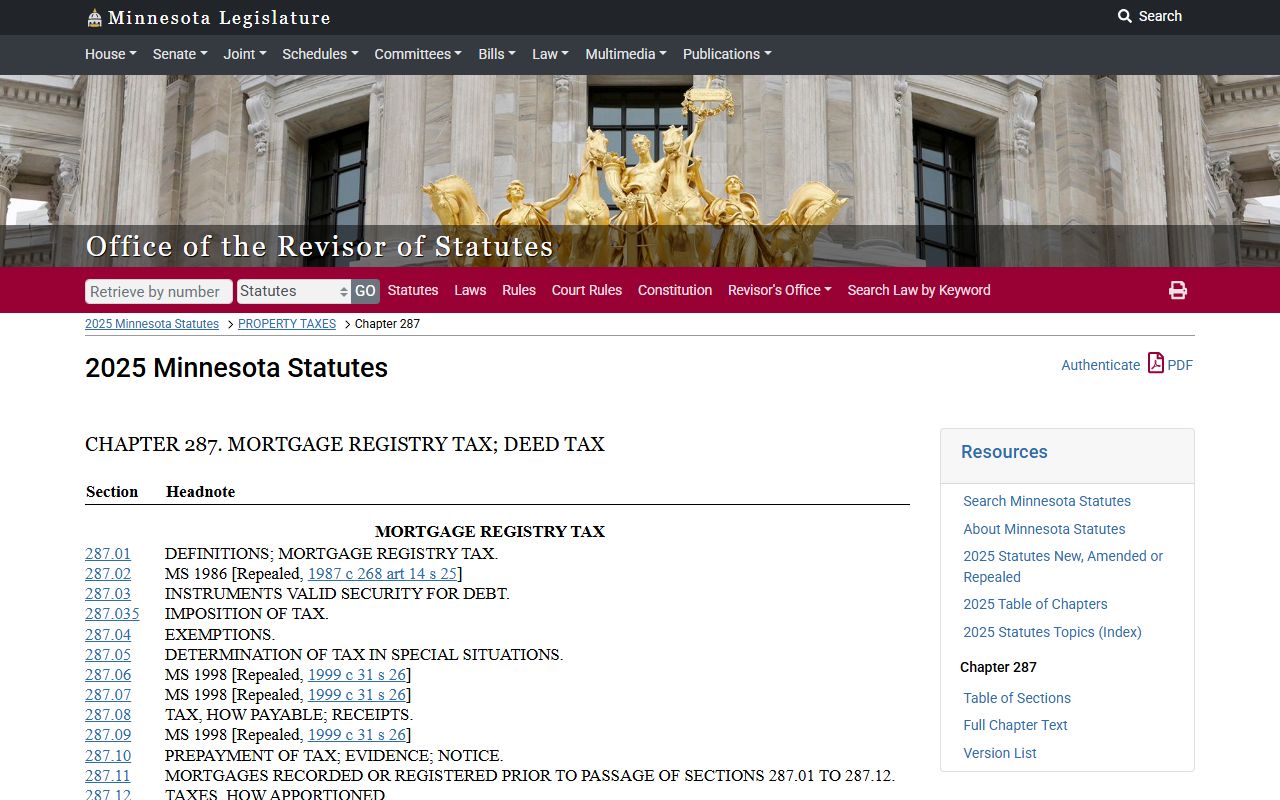

Two state-level transfer taxes apply when property changes hands. The State Deed Tax under Chapter 287 is 0.33% of the net consideration, with a minimum of $1.65 for any transfer. The tax is paid to the county at the time of recording. Transfers between spouses, to lineal family members, to government entities, and transfers under a divorce decree are exempt from deed tax. A Form S1 deed tax affidavit is required for taxable transfers with consideration over $1,000 and must be submitted with the deed at recording.

Chapter 287 of the Minnesota Statutes sets the deed tax and mortgage registry tax rates applied to property transfers and new mortgage recordings across the state.

The Mortgage Registry Tax under Chapter 287 is 0.23% of the principal debt secured by the mortgage. There is no maximum for residential or agricultural mortgages. Commercial and multi-housing mortgages are capped at $2,300 in mortgage registry tax.

Note: Recording fees and deed tax rates are set by state statute but collected at the county level. Contact the County Recorder where the property is located to confirm current fees before submitting documents.

Property Tax Refund for Minnesota Homeowners and Renters

Minnesota homeowners and renters may qualify for a Property Tax Refund from the Minnesota Department of Revenue. The refund is income-based. Homeowners with income under $119,790 can receive a refund up to $2,930. Renters with income under $64,920 can get up to $2,280. Claims are filed using Form M1PR and are typically due August 15. Refunds are issued after the state processes the claim. Full details and the form are at revenue.state.mn.us/property-tax-refund.

A special property tax refund is also available for homeowners whose net property tax increased more than 12% from one year to the next. The increase must be at least $100. There is no income limit for this special refund. The maximum is $1,000. Both types use Form M1PR and the same August 15 deadline. Renters file using rent certificates issued by their landlord, which show the portion of rent that counts as property tax paid.

Getting Copies of Minnesota Property Records

To get a copy of a recorded document, contact the County Recorder in the county where the property is located. Most offices can pull records by name, date range, or document type. Plain copies cost $1.00 to $2.00 per page at most counties. Certified copies cost $10.00 plus per-page fees and carry the official county seal. Some counties accept written mail requests. Others prefer in-person visits. Call ahead to confirm what the county allows before sending anything in.

For assessment data, start with the County Assessor or the Beacon property search portal. Beacon provides parcel maps, market values, sales history, and building information at no charge for basic searches. The Minnesota Department of Revenue publishes statewide data and county-level reports at revenue.state.mn.us. For well records, the Minnesota Department of Health maintains information at 651-201-4600 and at health.state.mn.us. The DNR manages state-owned land records and surplus land sales at dnr.state.mn.us/state_land.

Minnesota Well Disclosure and Property Records

When selling property in Minnesota that has a well, the seller must complete a Well Disclosure Certificate and record it with the County Recorder. The certificate lists every well on the property, including its type, status, and location. The recording fee for the certificate is $46.00 to $54.00 depending on the county. The seller must give the buyer a copy before closing. Failure to disclose wells can result in civil penalties up to $5,000 under Minnesota Statutes 103I.235. More information is at health.state.mn.us.

Wells are legal fixtures under Minnesota law. They transfer with the property. Sellers of homes with private wells must test for arsenic, lead, and coliform bacteria within one year before signing a purchase agreement. Other recommended tests include nitrate, manganese, and fluoride. Abandoned wells must be properly sealed by a licensed contractor. The Minnesota Department of Health's Well Management Section administers these rules and can be reached at 651-201-4600 or health.wells@state.mn.us. Information about selling a house with a private well is at health.state.mn.us/communities/environment/water/wells/sellinghouse.html.

Note: Well disclosure certificates are recorded with the deed at the county recorder's office and become part of the permanent property record for the parcel.

Browse Minnesota Property Records by County

Each of Minnesota's 87 counties has its own Recorder and Assessor. Pick a county below to find local contact info, search portals, and resources for property records in that area.

View All 87 Minnesota Counties

Minnesota Property Records by City

Residents of major Minnesota cities access property records through the Recorder and Assessor in their county. Pick a city below for local property records resources.